%20formatted-1.png?width=2528&height=739&name=SIGNiX%20Logo%20Main%20(white)%20formatted-1.png)

Credit unions have been issuing plastic cards for four decades. While EMV is a new twist, cards are old news compared to some other payments trends. Mobility is the current buzzword, and the mobile wallet may be poised to move from a curiosity to a mainstream contender in the consumer payments environment. No, cards are not going away, just like checks have not gone away. But, mobile payments are coming.

Mobile Payments Vs. Apple Pay

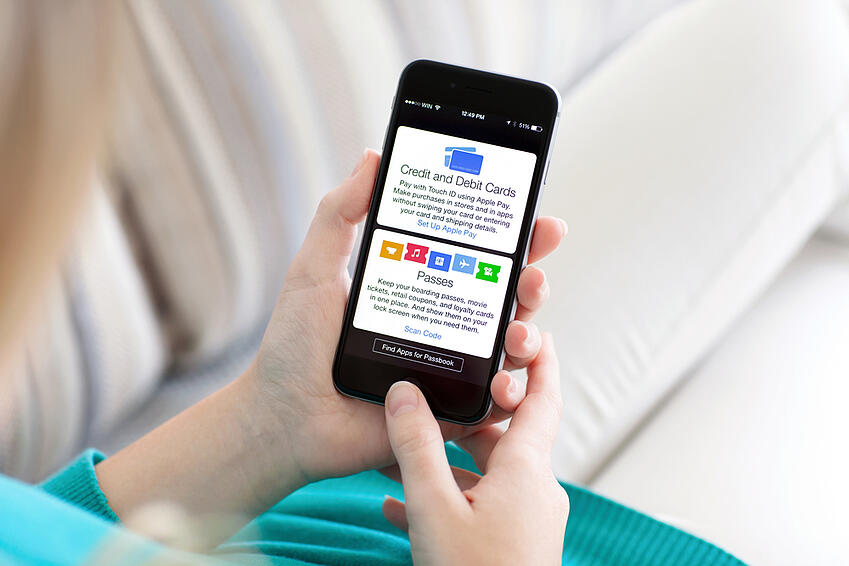

Starbuck’s mobile payments success among young people (and the young at heart) notwithstanding, mobile wallets weren’t going anywhere until the October 2014 release of Apple Pay.

The resulting numbers are staggering. Apple sold 10 million iPhone 6 devices in the first three days after the release. By mid-November, that number had doubled. In the roughly 30-days following the Apple Pay release, over 1 million consumers and over 500 financial institutions (72% of which were credit unions) had signed up.

What makes Apple Pay different?

Until Apple Pay, consumers had been wary of mobile payments because of security concerns. Apple Pay addressed their concerns with a two-pronged approach:

- Biometric identification enables users to complete transactions using a fingerprint sensor

- Device-specific tokenization—a credit card approval process between Apple and the user’s credit union, payment network or bank, which creates a device-specific Device Account Number

Apple holds a minority (40%) share of the mobile market (Android and Windows-based devices hold the remaining 60%), but Apple Pay may be a disruptive force in the acceptance of mobile payments, raising consumer confidence about security.

Should Your Credit Union Enroll in Apple Pay?

Almost 400 U.S. credit unions seem to think so Apple Pay is a good choice. Because the iPhone 6 is the only iPhone equipped with NFC chips, Apple Pay is only available on iPhone 6 and current generation iPads (for online purchases only). But the new release has certainly created a lot of press.

In deciding whether or not to enroll in Apple Pay, credit unions should be asking themselves these questions:

- How many of your members carry iPhones?

- How many will get a new phone in the next two years?

- If your members get a NFC-capable phone and your credit union is not in the wallet, who will they choose as their financial institution?

- What will be the cost of NOT signing up for Apple Pay?

- Apple Pay is not the only game in town. What about the 60% of consumers who prefer Android or Windows devices? Is your credit union going to be positioned to serve all of the options?

Many pundits believe you should jump on the Apple Pay bandwagon. The cost of going mobile will likely be high, but here’s the bigger question: Will the cost of NOT going mobile eventually be higher than the cost of going mobile?